Brexit and Liquidity Exits

In the United Kingdom, today was meant to be the long anticipated “Brexit Day”. As we write, it hasn’t happened and now appears to be postponed a little longer. In fact, we can’t really make head nor tail of what is going on with this pro-longed drama!

However, we have been thinking about how the changing geo-political landscape of the last three years has produced less certainty, unexpected outcomes and markets that can be counter-intuitive and hard to navigate. Adding to that, we have seen changing liquidity regimes across the markets we cover, significant for anyone in the business of pursuing best execution. Liquidity changes stemming from both major events and more subtle trends over time are challenging to deal with. Quote sizes can deteriorate and may no longer be what they used to be. Figuring that out in time and determining how you need to adapt is hard if you are executing manually or using unsophisticated algorithms. There is both an art and science to mastering evolving market dynamics and adapting execution strategies appropriately. This is a QB speciality.

There are a number of ways we measure liquidity, and three we focus on in particular. We measure liquidity using average quote size and average quote spread (a normalized measure of bid/offer spread especially useful for instruments with smaller tick sizes):

Average quote size = (bid size + ask size) / 2

Average quote spread = (ask – bid) / (0.5*(ask + bid))

We also use the Amihud liquidity measure using 1-minute intervals for the given time period, which is specifically defined as:

Illiquidity = Average ( |𝑟𝑡| / Volume𝑡 )

Where 𝑡 is one-minute intervals in our sample. The absolute return of each 1-minute bin is computed from mid price to mid price in order to avoid bid-ask bounce. The Amihud illiquidity as shown is essentially the measure the volatility in volume time. A higher number indicates less liquidity. It also provides a different perspective on analyzing liquidity. This measure of liquidity can be also thought of as cost of trading a unit dollar volume of the underlying instrument. This is a normalized measure and gives important information that is not captured by the quote size. While the quote size could shrink, unchanged Amihud liquidity levels would indicate that constant participation rate or VWAP algos would have similar slippage. This is crucial for QB’s Strobe algorithm. The shrinking quote size would nevertheless make it harder to trade a large size quickly, or to put it differently, one would get less trading done during the day when quote sizes are smaller. This is crucial for arrival price benchmark algos such as QB’s Bolt.

The plots below show the liquidity as measured by some of the above mentioned metrics for the Long Gilts and FTSE 100 futures measured using intraday trades and quotes and aggregated at the daily levels.

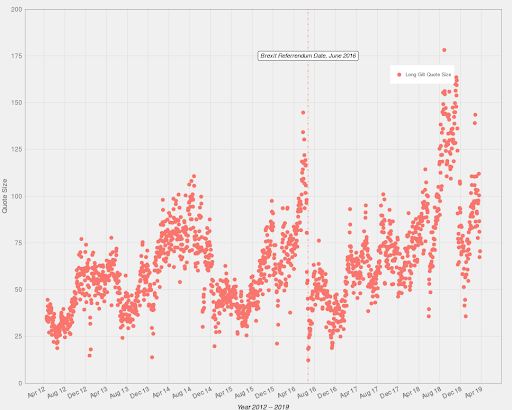

Long Gilts: Quote Size

Long Gilts: Quote Size

Long Gilts can be particularly challenging to trade at the best of times. Brexit does not make that any easier. The above chart shows the daily quote size of Long Gilt futures. The red dotted line is the Brexit referendum date, June 23, 2016. It can be clearly seen that the quote size shrank dramatically after the referendum.

FTSE 100: Quote Size

FTSE 100: Quote Size

A similar pattern can be observed for the FTSE 100 futures’ average daily quote size. The quote size went down around the referendum date but recovered after a few months. An interesting observation is that the quote size was shrinking for a few days prior to the referendum date in anticipation of the event. We have found similar patterns in other markets where quote size or other measures of liquidity have been useful for forecasting.

The two charts below show the Amihud illiquidity measure for the Long Gilt futures and FTSE 100 futures. Here the numbers are scaled and aggregated daily from the 1-minute return.

Long Gilts: Amihud Illiquidity

Long Gilts: Amihud Illiquidity

In the above chart, we can see a slight rise in the illiquidity of Long Gilt futures around the Brexit announcement date. However, overall the long term trend is that liquidity is increasing (illiquidity is decreasing). So while the quote size might have shrunk, the price impact would be lower for a small sized order.

FTSE 100: Amihud Illiquidity

FTSE 100: Amihud Illiquidity

For FTSE 100, the Amihud illiquidity has risen since the recent market sell off in December had a significant impact. However, prior to that it had been around the same levels for the last 6 years.

As can be seen that the Amihud liquidity has a slightly different pattern than the quote size. Analyzing liquidity does require some different perspectives in order to reach a thorough conclusion. This is why we will often look at both quote size and the Amihud illiquidity measure. In our research, we also look at the inverse relationship between liquidity and volatility over time. Whilst the result would not surprise any trader, as this is quite well understood, what is fascinating is the leading indicator that liquidity can have over forthcoming volatility in the market. This was particularly evident in the deterioration of liquidity prior to the volatility of February 2018, and remains something worth keeping an eye on, particularly in the UK where the Brexit drama is not over yet.

Changes in liquidity can occur slowly, accompanying broader market moves, more medium term around increased volatility, or they can be very specific intra-day changes, for example around an FOMC announcement. We show in one of our research papers the impact of the December 19, 2018 FOMC announcement on the liquidity of major asset classes such as interest rates, equity and crude oil. The liquidity drop was dramatic across all the asset classes; however, the drop was most severe (at almost 50%) for the Ten Year futures. FOMC announcements are usually quite impactful on liquidity but the effect of some can be multiples of others. For example, September 26, 2018, saw only a 10% drop in liquidity in Ten Year futures.

Read more of our Research team’s papers on liquidity:

– Recent Changes in E-Mini S&P 500 Futures’ Market Microstructure: An Update (February 1, 2019)

– Recent Changes in Commodity Futures’ Market Microstructure (January 7, 2019)

– Recent FOMC Announcement and Changes in Futures’ Market Microstructure (January 3, 2019)

–Recent Changes in Crude Oil Futures’ Market Microstructure (December 10, 2018)

– Recent Volatility and Changes in Futures Market Microstructure (April 10, 2018)

Quantitative Brokers

London

March 29, 2019