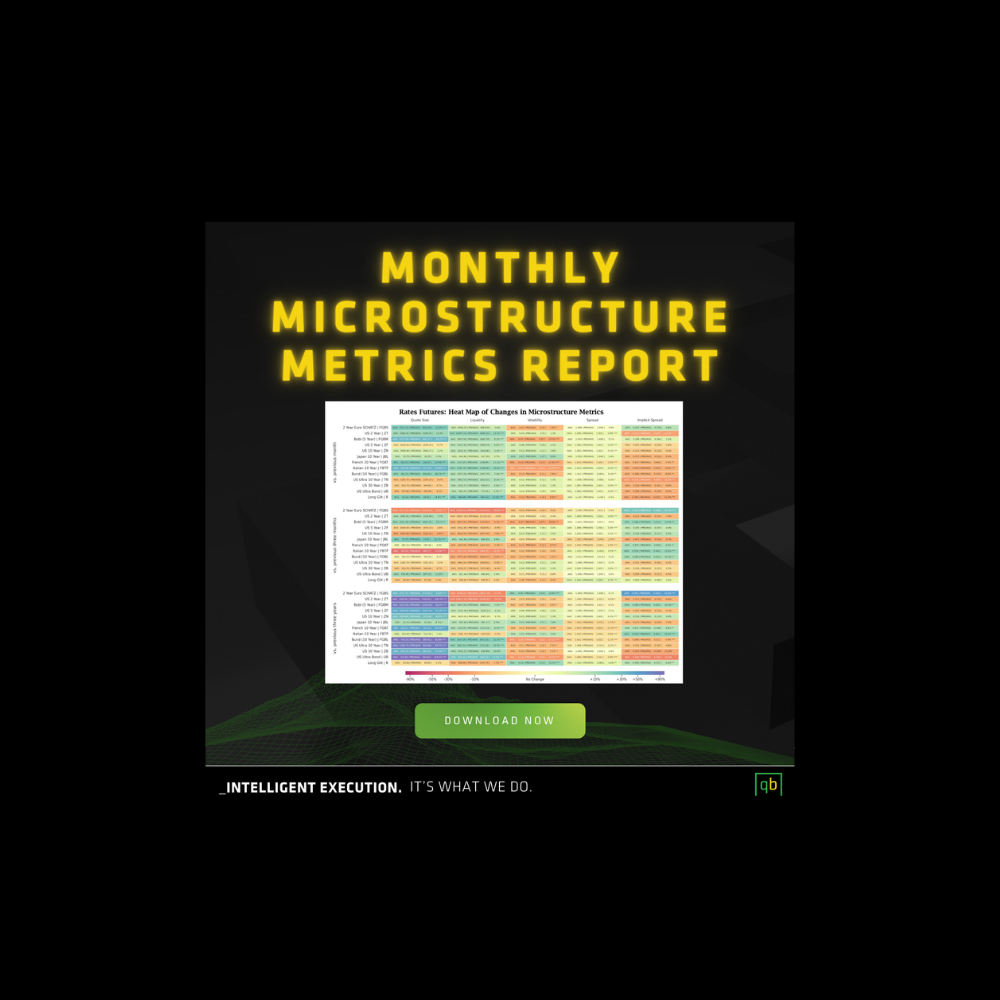

MONTHLY MICROSTRUCTURE METRICS REPORT: JUNE 2026

July 6, 2026

We analyzed the recent changes (June 2026) in market microstructure metrics for interest rate, equity, VX, energy, agriculture, and metal futures and compared these against historical averages. The definitions of these microstructure metrics are provided below...

Read More

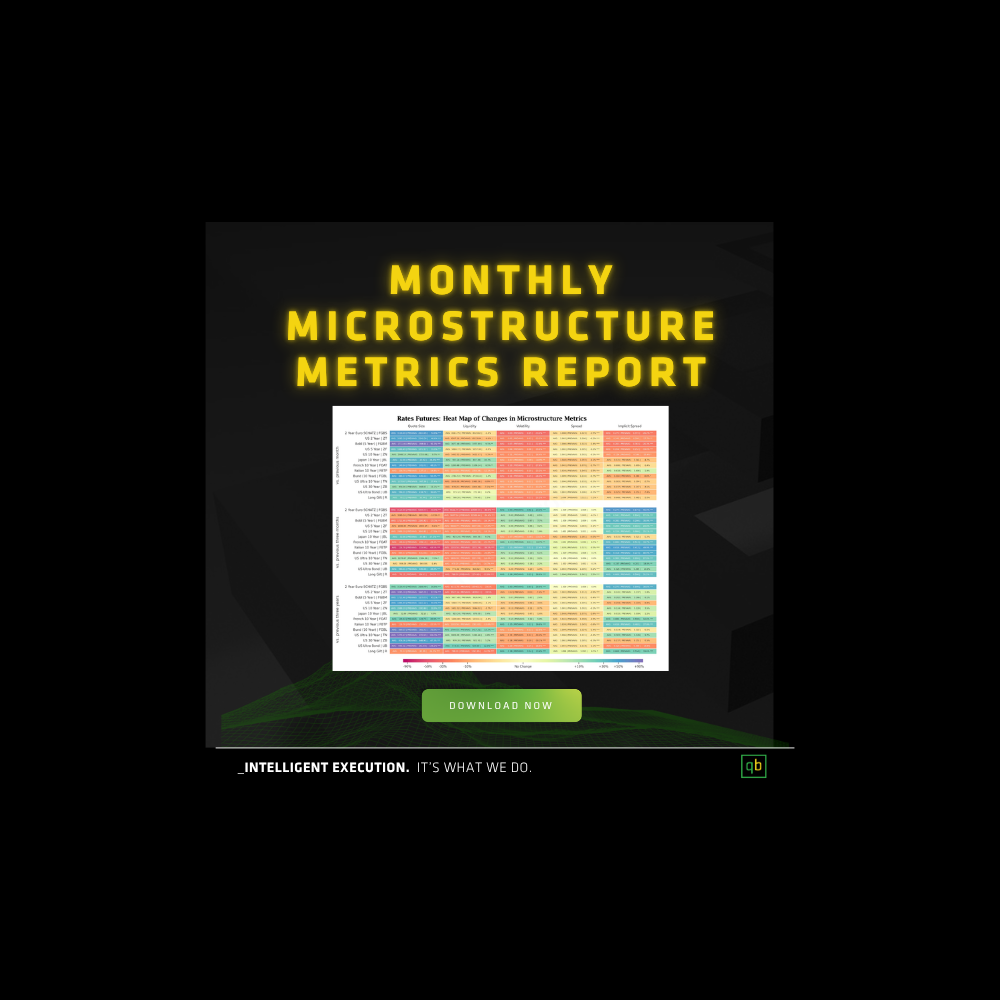

MONTHLY MICROSTRUCTURE METRICS REPORT: MAY 2026

June 8, 2026: We analyzed the recent changes (May 2026) in market microstructure metrics for interest rate, equity, VX, energy, agriculture and metal futures and compared these against historical averages. The definitions of these microstructure metrics are provided on the next page...

Read More

MONTHLY MICROSTRUCTURE METRICS REPORT: APRIL

May 5th, 2026 - We analyzed the recent changes (April 2026) in market microstructure metrics for interest rate, equity, VX, energy, agriculture and metal futures and compared these against historical averages. The definitions of these microstructure metrics are provided on the next page.

Read More

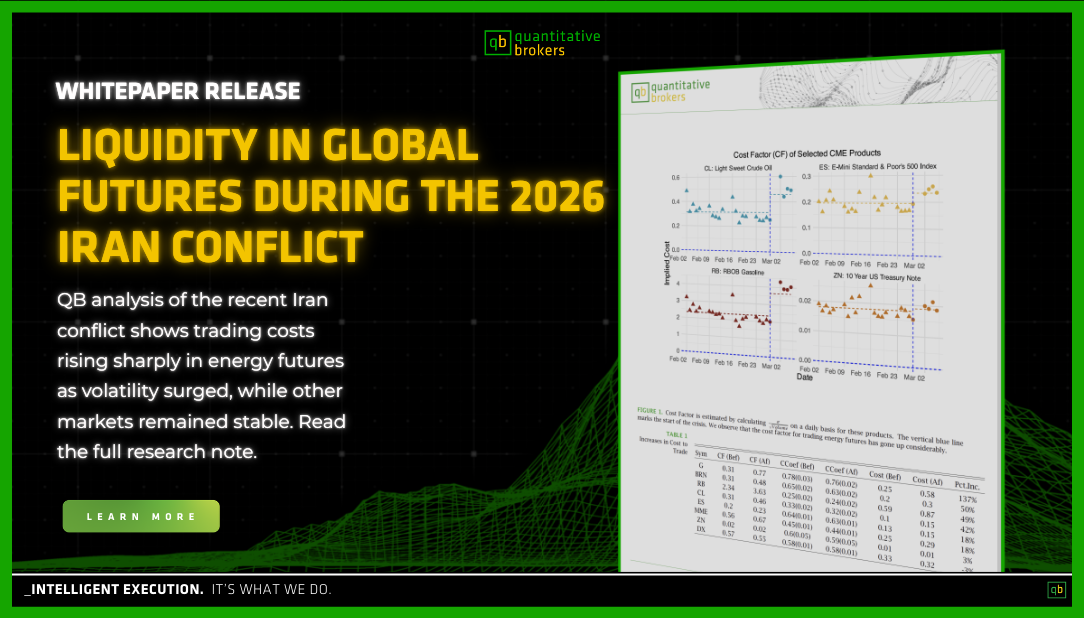

Futures Microstructure During The 2026 Iran Conflict

April 10th, 2026 - Building on our early-March publication [SA26], we revisited trading conditions using the full month of March data. This update maintains the same framework, metrics, and presentation format to ensure direct comparability with our initial findings. As shown in Figure 1-4, we continue to observe elevated trading costs across most futures products relative to pre-conflict conditions. The broader March dataset confirms that the initial dislocations identified in early March were not transient but persisted throughout the month, albeit with some normalization in select markets.

Read More

Liquidity in global futures during the 2026 Iran conflict

March 9th, 2026 - Using QB’s cost model as well as our recent realized results, we can see a clear increase in trading costs across energy products last week. G, BRN, RB, CL, ES and MME show cost increases of 20-140%. These changes are largely in line with the increase in realized volatility.

Read More

Monthly Microstructure Report July 2025

August 6th, 2025 - In this paper, we analyze liquidity in June compared to July. Liquidity improved in July for interest rate and major equity index futures, especially VIX, with larger quote sizes and lower volatility.

Read More

Predicting Fill Ratios For Cash Treasury Venues

June 27th, 2025 - QB employs a tie-break algorithm in its Smart-Order-Router (SOR) to determine the optimal venue for sending aggressive cash treasury orders when multiple venues offer the best price.

Read More

SOR Passive Placement Enhancement For Cash Treasuries

June 12th, 2025 - In this paper, we propose a new model for passive order placement in smart order routing (SOR) for cash treasuries, designed to improve the estimation of order fill times and thereby enable more effective size allocation across venues by minimizing time to fill.

Read More

Passive Slice Sizing Tactics For Schedule Algorithms In Pro-Rata Markets

May 13th, 2025 - In this note, we illustrate a specific difficulty that arises when posting passively in markets that use a pro-rata matching policy, such as CME treasury calendar spreads.

Read More

Basis Trading: Maximizing Our Hit Rates Across U.S. Treasuries Cash

April 10th, 2025 - This whitepaper examines the optimal wait time for executing basis trades in U.S. treasuries cash and futures markets.

Read More

Opportunistic Crossing In Cash Treasuries

January 3rd, 2025 - We outline a simple strategy to make crossing decisions based on the dynamics of the bid-ask spread, comparing its current value to forecast future values.

Read More

Trends In Market Volumes Around Christmas And The New Year Period

December 17th, 2024 - We analyze trends in volumes over the late December period covering Christmas and the New Year. Typically, market volumes drop sharply during this period and so it is important to be aware of this when planning trades. This note is intended as a guide for such planning with the expectation that the same volume patterns will occur this year.

Read More

US Treasuries Smart-Order-Routing (SOR) For Aggressive Crosses

November 8th, 2024 - We implement a new logic for the On-The-Run Treasuries Smart Order Router (SOR) for aggressive crosses, which allocates quantities across venues based on a ranking algorithm that uses the venues’ market impact and fill ratio.

Read More

Trading Small-Tick Contracts

November 5th, 2024 - In the spring of 2024, QB began a project to improve algorithm behavior, especially for small-tick assets: those with bid-ask spread larger than the minimum price increment, and with thin order books having small size and few orders.

Read More

CME Rates Calendar Spread Cointegration And Other Roll Improvements

July 17th, 2024 - We recently improved our algo performance in rolls by fine-tuning our aggressive cross signal and improving our accuracy in tracking our queue position. Read more.

Read More

Regime-based Optimal Passive Limit Order Placement

July 17th, 2024 - QB’s algos combine market state identification in real-time with fill probability for dynamic limit order placement and other hyperparameters for order placement.

Read More

Asset Manager's Position Of 10-Year Treasury Futures And Calendar Spread Changes

February 25th, 2024 - The net asset manager’s (AM) position of the U.S. 10-year futures from the Commitment of Traders (COT) report is at a 3-year high. The Figures show credibility to our roll forecasts model.

Read More

Cash Treasury Month-End Profiles Around 4:00 P.M. Benchmark Timing

January 25th, 2024 - In this article, we will mainly look at month-end intra-minute volume profiles of Cash Treasury around the benchmark timing of 4:00 p.m. Eastern Time. Additionally, we also analyze the price profiles around the benchmark timing.

Read More

Block Trades Against QB Algos: Evidence From EUREX Interest Rate Calendar Spreads

November 20th, 2023 - Our recent research examines how block trades impact futures markets and interest rate product calendar spreads.

Read More

Robust Fitting

September 15th, 2023 - This paper provides comprehensive details of robust regression, which was referenced in our previous paper, "Robust Cost Modeling."

Read More