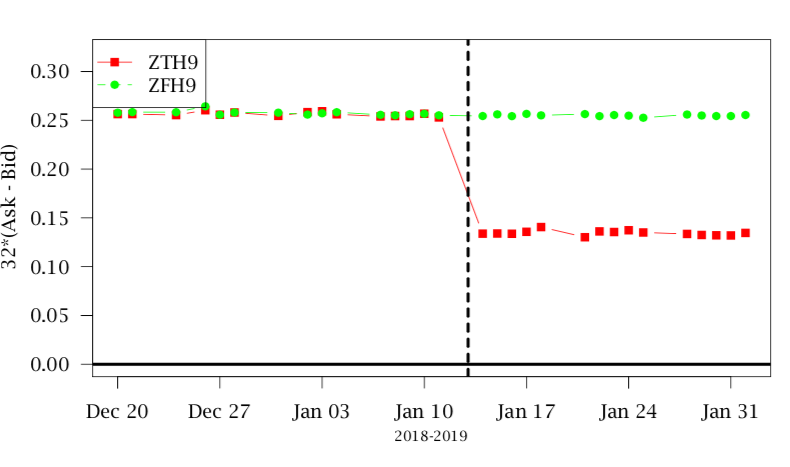

Impact of Tick Size Reduction on Market Microstructure: Implications for ASX Roll Periods

August 31, 2020 - In this paper, we analyze the potential impact of tick size (minimum price increment) changes for the upcoming ASX roll period. ASX will reduce the tick size of the 3-Year and 10-Year interest rate futures during the 5 days of the roll period in September 2020. Specifically, the 3-Year tick size will go from 1/2𝑛𝑑 to 1/5𝑡h basis point, and the 10-Year tick size will change from 1/4𝑡h to 1/10𝑡h basis point during the roll period.

Read More

Implied Quotes for Options On Futures

August 21, 2020 - In this white paper, we introduce the notion of implied quotes to address this problem and also present a fast approximation algorithm to generate the best prices of implied quotes in real-time.

Read More

Liquidity and Quote Size Changes in Futures

August 7, 2020 - We look at the most traded symbol for several instruments across different exchanges to report the average daily quote size and liquidity of July 2020. We compare the same against the liquidity and quote size of June 2020 as well as July 2019.

Read More

Transaction Cost Model in March 2020

April 24, 2020 - During March 2020, market volume and volatility increased dramatically, because of the uncertainty about the economic impact of the Covid-19 virus.

Read More

Volatility, Multidimensional Regimes and Execution Performance

March 23, 2020 - QB’s research to identify regimes using multidimensional inputs and machine learning to optimize execution. Our methodology provides a blueprint for how to combine algorithmic strategies to drive down costs even in challenging times.

Read More

Mass Quote Protection

October 14, 2019 - While certainly not the case with every order, frequent liquidity takers in the CME’s options on futures markets are likely familiar with “vanishing liquidity.”

Read More

Cointegration As a Price Forecast

July 29, 2019 - The topic of cointegration is not new to finance literature. The hypothesis of cointegrated bond prices has been thoroughly examined by several authors.

Read More

Augmented Volume Measurement for Participation Rate Limits

April 25, 2019 -When using algorithms to work meta-orders on electronic markets, traders often want to place controls on the algorithm in order to limit the market impact.

Read More

Trade at Settlement (TAS)

April 23, 2019 - Trade-at-Settlement (TAS) on the CME is a listed futures instrument. It permits market participants to trade at a differential to the underlying futures, current day, not-yet-known settlement price.

Read More

Forecasting U.S Treasury Futures' Calendar Spread During The Roll Period

November 15, 2018 - We continued our previous study and this time we describe additional variables added to forecast the ten days of the roll period, we also outline our multivariate model used in our forecasts.

Read More

Machine Learning For Limit-Order Routing in Cash Treasury Markets

June 12, 2018 - Cash Treasuries, unlike most products traded by QB, are available to trade on multiple venues.

Read More

Recent Volatility and Changes In Futures Market Microstructure

April 10, 2018 - Market microstructure and liquidity profiles have important implications for the price impact and slippage of client orders.

Read More

Intra-Day Price Bubbles

January 16, 2018 - In recent years, the topic of price or economic bubbles has received significant attention.

Read More

Inter-Commodity Spreads and Implied Pricing

February 10, 2017 - Implied quoting is a characteristic feature of interest rate futures markets.

Read More

Market Impact and Alpha

January 13, 2017 - Price impact caused by an aggressive order is a staple of market microstructure research.

Read More

Multidimensional Futures Rolls

December 15, 2018 - Price impact caused by an aggressive order is a staple of market microstructure research.

Read More

Humans: Are we that predictable?

November 12, 2016 - We are often asked at QB if algorithms are always better than humans. It might surprise the reader that we don’t see this as an “us” vs “them”.

Read More

Hidden Liquidity in CME Futures

September 15, 2016 - Hidden liquidity is resting volume available in the order book, that is not visible in market data but that can be traded against by a suitable marketable order.

Read More

QB Simulator Performance

November 4, 2016 - QB’s execution simulator is an important tool for developing and evaluating our algorithms.

Read More

1-Minute Bin Volume Forecast Model

September 14, 2016 - In response to strong client demand, Quantitative Brokers (QB) has developed a new algorithm called Closer benchmarked to the daily settlement price.

Read More