June 22, 2021 - In our recent whitepaper “Intraday Liquidity Profiles of Bitcoin Futures and Micro Bitcoin Futures” we analyzed the intraday profiles of BTC futures and compared them against the liquidity of the MBTC.

Read More

June 22, 2021 - In our recent whitepaper “Intraday Liquidity Profiles of Bitcoin Futures and Micro Bitcoin Futures” we analyzed the intraday profiles of BTC futures and compared them against the liquidity of the MBTC.

Read MoreJune 7, 2021 - In this whitepaper, we show the Bayesian adjustments and the results of our volume forecast model to accommodate the shift in benchmark timing for Bloomberg Barclays US Aggregate Bond Index.

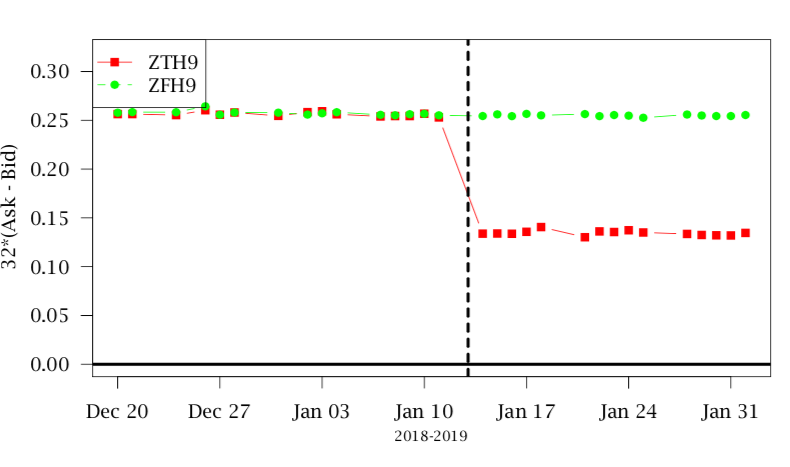

Read MoreMay 10, 2021 - In this whitepaper, we examined the changes in the microstructure of STOXX Banks futures (FESB) to analyze the potential impact of the tick size reduction of STOXX 50 futures (FESX).

Read MoreApril 7, 2021 - In this paper we examine the impact of tick size changes on Eurex DAX Index Futures (DAX) outrights’ microstructure variables.

Read MoreMarch 24, 2021 - In this paper we measure schedule-based algo execution performance by looking beyond slippage against benchmarks, and trading speed metrics, in order to verify if the realized schedule was fast or slow.

Read MoreFebruary 23, 2021 - In this paper, we describe our machine learning technique of an unsupervised Neural Network method to cluster instruments.

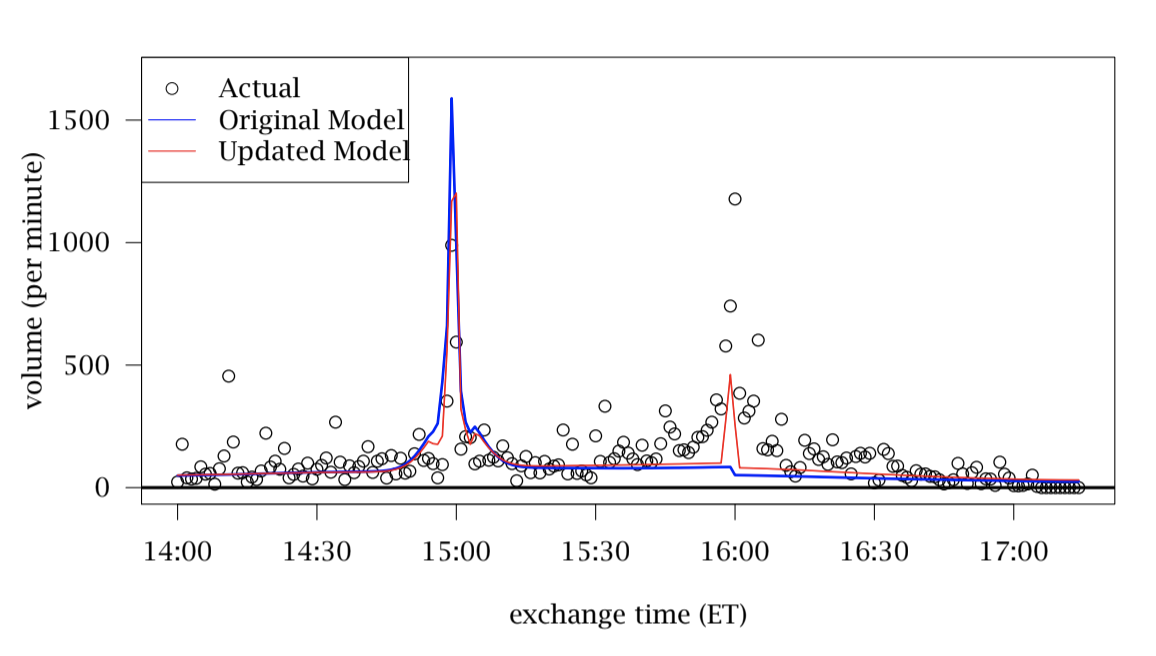

Read MoreJanuary 25, 2021 - In this paper, we present a regression-based methodology to improve the volume predictions during the continuous hours and specific events such as the settlement window.

Read MoreJanuary 26, 2021 - In this paper, we outline our approach to adjust for the end of the month days for the 10-year and 30-year Cash Treasury. The method is similar to other instruments as well.

Read MoreDecember 22, 2020 - This paper summarizes recent updates on three key components of the Closer algorithm. QB's Closer is an alternative way of targeting settlement price. The Algo incorporates an intelligent combination of price and volume forecast along with an optimization technique for order placement.

Read MoreNovember 12, 2020 - In this article, we analyze the changes in the term structure after the election. The findings are interesting as the level of VIX has dropped whereas the implied volatility term structure of options on E-mini S&P 500 futures indicates the possibility of an extreme movement.

Read MoreOctober 29, 2020 - In this paper, we use end-of-day data of VIX futures, options on E-mini S&P 500 futures and options on 10-Year Treasury to analyze the uncertainty related to the upcoming presidential election.

Read MoreOctober 8, 2020 - In this paper, we propose a simple model for summarizing historical trade performance in futures markets.

Read MoreAugust 31, 2020 - In this research, we compare the microstructure variables of ASX 3-Year and 10-Year calendar spreads during the September roll period against the previous roll periods.

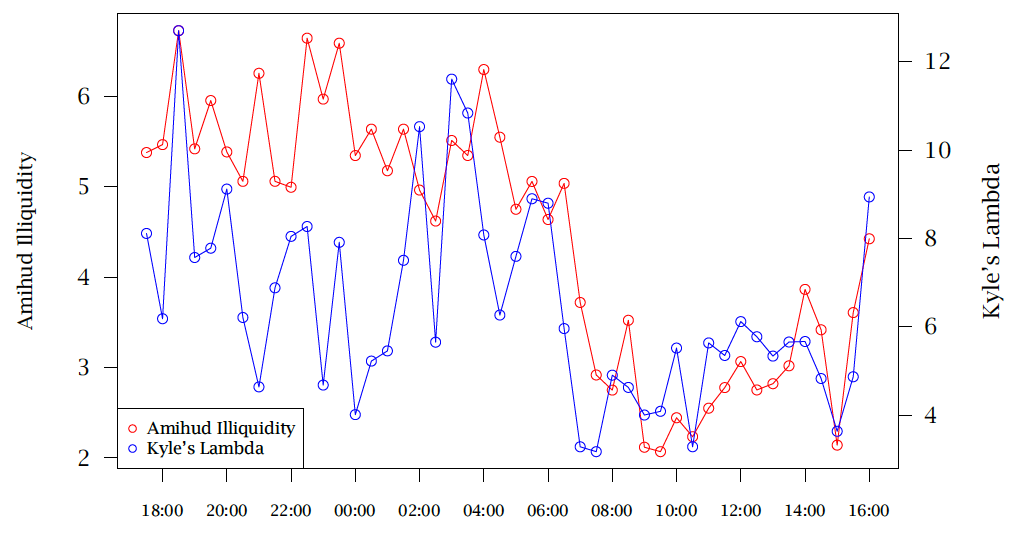

Read MoreSeptember 24, 2020 - In this paper, we apply the causal forest, a semi-parametric estimator for causal effects, to identify the impact—precisely, the partial effect—of order and trade size on price, as well as how these impacts vary with market conditions.

Read MoreAugust 31, 2020 - In this paper, we analyze the potential impact of tick size (minimum price increment) changes for the upcoming ASX roll period. ASX will reduce the tick size of the 3-Year and 10-Year interest rate futures during the 5 days of the roll period in September 2020. Specifically, the 3-Year tick size will go from 1/2𝑛𝑑 to 1/5𝑡h basis point, and the 10-Year tick size will change from 1/4𝑡h to 1/10𝑡h basis point during the roll period.

Read MoreAugust 21, 2020 - In this white paper, we introduce the notion of implied quotes to address this problem and also present a fast approximation algorithm to generate the best prices of implied quotes in real-time.

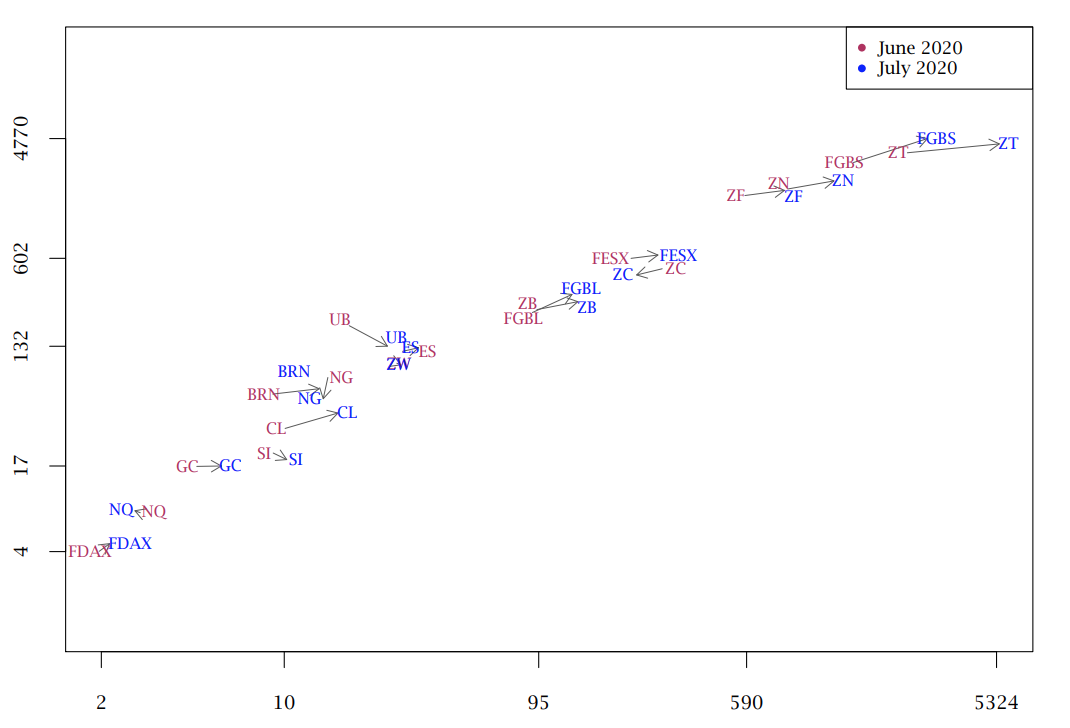

Read MoreAugust 7, 2020 - We look at the most traded symbol for several instruments across different exchanges to report the average daily quote size and liquidity of July 2020. We compare the same against the liquidity and quote size of June 2020 as well as July 2019.

Read MoreApril 24, 2020 - During March 2020, market volume and volatility increased dramatically, because of the uncertainty about the economic impact of the Covid-19 virus.

Read MoreMarch 23, 2020 - QB’s research to identify regimes using multidimensional inputs and machine learning to optimize execution. Our methodology provides a blueprint for how to combine algorithmic strategies to drive down costs even in challenging times.

Read MoreOctober 14, 2019 - While certainly not the case with every order, frequent liquidity takers in the CME’s options on futures markets are likely familiar with “vanishing liquidity.”

Read More